Why European Savers Are Searching for Better Returns

For most of the last decade, European savers had one realistic option: accept near-zero interest from their bank and watch inflation quietly eat their savings. That changed when the European Central Bank raised rates aggressively between 2022 and 2024. Suddenly, savings accounts started paying something again.

But rates have been shifting. The ECB began cutting in 2024, and many banks have already passed those cuts on to depositors faster than they passed on the hikes. If you opened a high-yield account in 2023, your rate today is probably lower than you expected.

That gap between what banks offer and what your money could earn elsewhere is exactly why more European savers are looking at alternatives, including DeFi-powered platforms that operate outside the traditional banking system entirely.

This article compares the most realistic options available to European savers in 2026: traditional banks, neobanks, and DeFi platforms. We look at actual rates, how accessible each option is, and what risks you are actually taking on.

How We Compared These Options

We focused on four things that matter to everyday savers:

- APY (Annual Percentage Yield): what you actually earn after compounding

- Liquidity: can you access your money when you need it?

- Fees and lockups: are there hidden costs or minimum holding periods?

- Transparency: can you verify where your money is and what it is doing?

We did not include products that require you to lock funds for 12 months or more, since most savers want flexibility. We also excluded products only available in one or two countries unless they are widely accessible across the EU.

Traditional Banks: The Familiar Option

Big Banks Still Lag Behind

The major retail banks across Europe—think Deutsche Bank, BNP Paribas, ING, Santander—still offer savings rates that trail inflation in most countries. As of early 2026, most big-bank savings accounts in the eurozone pay between 1.5% and 2.5% APY on standard savings products.

Some banks offer promotional rates for new customers, often 3% to 3.5% for the first three to six months, before dropping back to their standard rate. These teaser rates look good on paper but require you to actively switch accounts every few months to keep up, which most people do not do.

The main advantage of a big bank is familiarity and deposit insurance. In the EU, deposits up to 100,000 euros are protected under the Deposit Guarantee Schemes Directive. That protection is real and meaningful.

Government-Backed Savings Schemes

Several European countries offer state-backed savings products with regulated rates. France has the Livret A, currently paying 2.4% APY, tax-free, with instant access. Germany has no direct equivalent but offers Tagesgeld (overnight money) accounts through regulated banks. The Netherlands has spaarrekeningen through banks like Rabobank and ABN AMRO.

These products are safe and accessible, but the rates are set by governments or central banks, not markets. When rates fall, your return falls with them, and you have no say in the matter.

Neobanks and Online Savings Platforms

Revolut Savings Vaults

Revolut offers savings vaults that pay interest on euros, pounds, and other currencies. Rates vary by plan tier. As of 2026, Revolut Metal and Ultra subscribers can access rates around 3.5% to 4% on EUR balances. Standard plan users get significantly less.

The catch is that the best rates are tied to paid subscription plans costing between 8 and 45 euros per month. If you are not already paying for Revolut for other reasons, the math on whether the higher interest rate actually nets you more money depends entirely on your balance size.

Revolut holds customer funds in regulated money market funds or partner banks, depending on the product. It is not a bank itself in most EU jurisdictions, though it received a European banking licence in 2024.

Trade Republic and Scalable Capital

Trade Republic became well known in Germany and across Europe for offering 4% interest on uninvested cash, paid as a daily accrual. That rate has since come down as ECB rates fell. As of early 2026, Trade Republic pays around 3% on cash balances up to 50,000 euros.

Scalable Capital offers a similar product through its broker platform, with rates around 2.5% to 3% depending on account type.

Both platforms are regulated, offer deposit protection, and are genuinely easy to use. The limitation is that they are primarily investment platforms, and the savings rate is a secondary feature, not the core product. Rates can change with little notice.

DeFi Savings Accounts: How They Work

What Is a DeFi Savings Account?

DeFi stands for decentralized finance. Instead of depositing money with a bank that lends it out at its own discretion, DeFi protocols let you deposit funds directly into smart contracts that manage lending according to transparent, publicly auditable rules.

The key difference from a traditional bank: everything happens on a blockchain. Every deposit, every loan, every interest payment is recorded publicly and can be verified by anyone. There is no head office deciding what to do with your money behind closed doors.

The most common DeFi savings approach involves stablecoins, digital assets pegged to the US dollar or euro. USDC is the most widely used dollar-pegged stablecoin, issued by Circle and regularly audited. When you deposit into a DeFi savings product, your euros or crypto are often converted to USDC, which is then deployed into lending protocols.

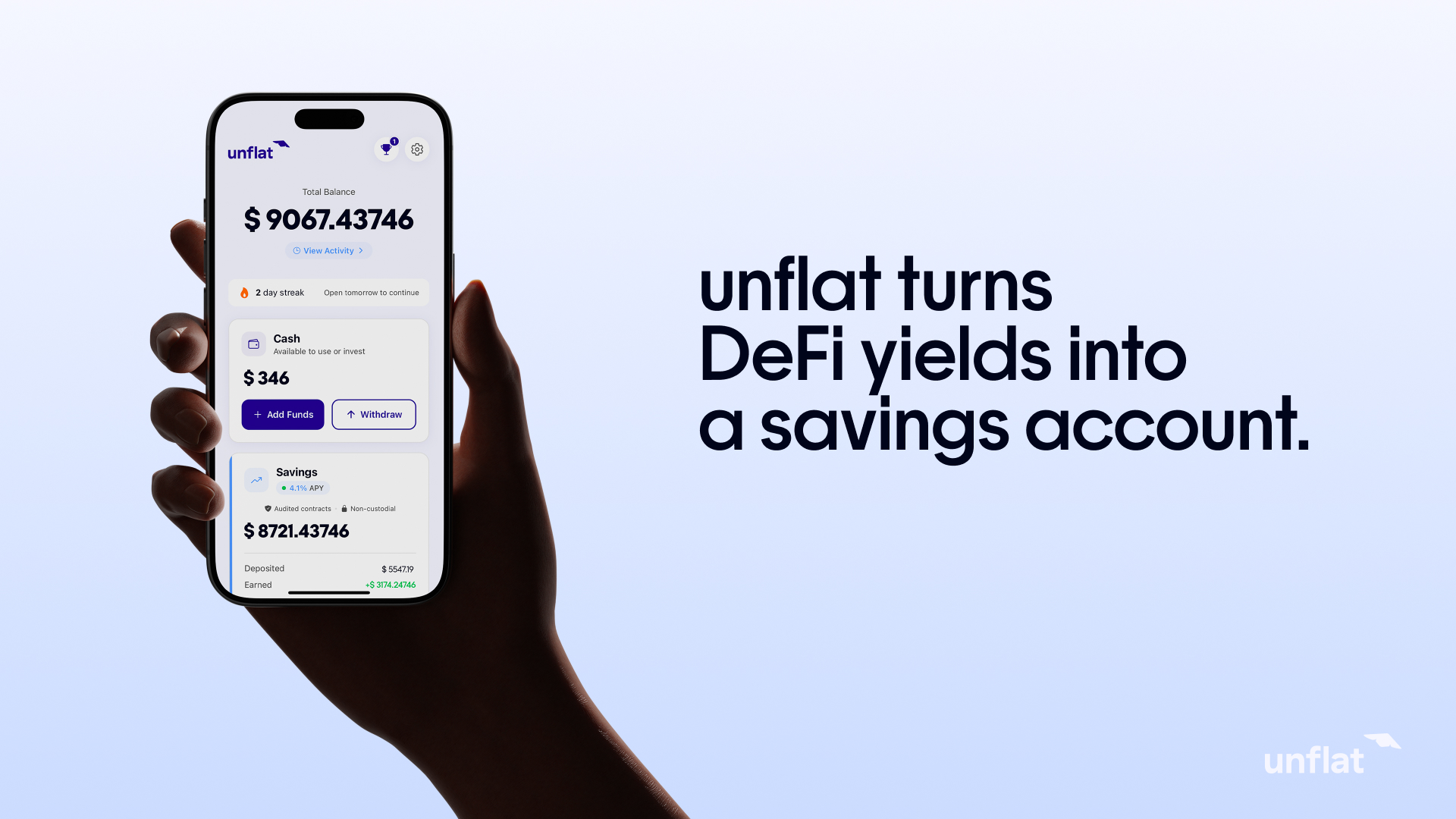

How unflat Works

unflat.finance is built specifically for European savers who want access to DeFi yields without needing to understand blockchain infrastructure.

Here is how it works in plain terms:

- You deposit money via bank transfer or crypto

- Your deposit is converted to USDC

- That USDC is deployed into Morpho Protocol, a decentralized lending market

- Borrowers on Morpho must pledge more collateral than they borrow (overcollateralized lending), which protects lenders from default

- Interest accrues daily

- You can withdraw at any time with no fees and no lockup period

Every transaction is recorded on-chain, meaning you can verify exactly where your money is and what it is earning at any time. You are not trusting a bank's quarterly report. You are reading a public ledger.

The yield on unflat comes from real borrowing demand in the Morpho Protocol market. It is not a promotional rate, and it is not subsidized by a company hoping to attract users. It reflects what borrowers are actually paying to access liquidity.

Side-by-Side Comparison: APY, Access, and Risk

| Option | Approximate APY (Early 2026) | Instant Access? | Deposit Insurance? | Transparency |

|---|---|---|---|---|

| Big EU banks (standard) | 1.5% to 2.5% | Yes | Yes (up to 100k EUR) | Low |

| Livret A (France) | 2.4% | Yes | Government-backed | Low |

| Trade Republic | ~3% | Yes | Yes (up to 100k EUR) | Low |

| Revolut (Metal/Ultra) | ~3.5% to 4% | Yes | Partial (varies) | Low |

| unflat (Morpho Protocol) | Variable, market-driven | Yes | No traditional insurance | Full on-chain |

The APYs for traditional and neobank products are relatively stable but move with ECB policy. The DeFi yield through unflat is market-driven, meaning it can be higher or lower depending on borrowing demand. Historically, USDC lending yields on protocols like Morpho have ranged from 4% to 10%+ during periods of high demand.

The "no traditional insurance" row for unflat is important and covered in the next section.

What Are the Real Risks?

Traditional Bank Risks

The main risk with traditional banks is not that they will collapse. It is that your real return after inflation is low or negative. If inflation runs at 2.5% and your savings account pays 2%, you are losing purchasing power every year, slowly and quietly.

There is also rate risk. Banks can lower rates at any time. The 3% you signed up for can become 2% within months, and there is nothing you can do except switch accounts.

Deposit insurance protects you up to 100,000 euros per bank per person. Above that threshold, you have real counterparty risk if a bank fails.

DeFi Risks

DeFi carries different risks that you should understand clearly before using any platform.

- Smart contract risk: The code running Morpho Protocol could have a bug or vulnerability. Morpho is one of the most audited protocols in DeFi, with multiple independent security reviews, but no code is perfectly risk-free.

- Stablecoin risk: USDC is backed by US dollars held in regulated financial institutions and is audited regularly by Deloitte. It has maintained its dollar peg reliably. But it is not government-insured. In an extreme scenario, Circle (the issuer) could face regulatory or operational problems.

- Variable yield: The interest rate is not fixed. It moves with market demand. This is different from a savings account with a stated rate.

- Currency exposure: If you are a euro-based saver, your deposit is converted to USDC (a dollar-denominated asset). If the euro strengthens significantly against the dollar, your returns in euro terms could be reduced.

unflat is transparent about these risks. The on-chain nature of the product means you can see exactly what is happening with your funds at all times, which is more than most banks offer.

Who Should Use Which Option?

Use a traditional bank or Livret A if:

- You want government-backed deposit insurance on your full balance

- You are uncomfortable with anything outside the regulated banking system

- Your balance is large enough that the 100,000 euro insurance cap matters

Use Trade Republic or Revolut if:

- You already use these platforms for investing or payments

- You want a simple, regulated product with decent rates and no extra setup

- You are comfortable with rates that move with ECB policy

Use unflat if:

- You want a higher potential yield and are comfortable with the different risk profile

- You value full transparency about where your money is and what it earns

- You want daily interest accrual with no lockups or withdrawal fees

- You are curious about DeFi but do not want to manage wallets, gas fees, or protocol interfaces yourself

Many savers in 2026 are not choosing just one option. Keeping some funds in an insured bank account and some in a DeFi platform like unflat.finance is a practical way to balance safety and yield.

Frequently Asked Questions

There is no single best option because it depends on your priorities. If you want deposit insurance and simplicity, Trade Republic at around 3% or Revolut Metal at 3.5% to 4% are strong choices. If you want higher potential yields with full transparency and no lockups, a DeFi platform like unflat.finance is worth considering. Many savers use a combination.

DeFi carries different risks from traditional banking, including smart contract risk and no government deposit insurance. However, platforms like unflat use overcollateralized lending through Morpho Protocol, which means borrowers must pledge more than they borrow. Every transaction is publicly verifiable on-chain. It is not risk-free, but the risks are transparent and specific, not hidden.

unflat deposits your funds into Morpho Protocol, a decentralized lending market. Borrowers pay interest to access liquidity, and that interest flows back to depositors. Because borrowers must overcollateralize their loans, the system has built-in protection against default. The yield reflects real borrowing demand, not a promotional rate.

Yes. unflat has no lockup periods and no withdrawal fees. Interest accrues daily, and you can access your funds whenever you need them.

USDC is a stablecoin issued by Circle, pegged to the US dollar and backed by dollar-denominated assets held in regulated financial institutions. It is audited regularly. unflat uses USDC because it is the most liquid and widely used stablecoin in DeFi lending markets, which is where the yield comes from.

unflat accepts deposits via bank transfer and crypto, making it accessible to savers across Europe. You can check current availability and supported deposit methods at unflat.finance.

The Livret A currently pays 2.4% APY, is tax-free, and is government-backed. It is one of the safest savings products available in France. DeFi platforms like unflat can offer higher yields, but without government insurance and with variable rates. The right choice depends on whether you prioritize safety or yield potential.

Make Your Savings Work Harder

European savers in 2026 have more options than at any point in recent memory. Traditional banks have improved their rates from the near-zero era, neobanks offer competitive products with good user experience, and DeFi platforms now make it possible to access lending market yields without technical expertise.

The honest answer is that no single product is right for everyone. Know what you are optimizing for: safety, yield, flexibility, or transparency. Then match the product to your actual priorities.

If you want to explore what DeFi-powered savings looks like in practice, unflat.finance is a straightforward starting point. No wallets to manage, no lockups, and every transaction verifiable on-chain.

Start earning with unflat

Access DeFi yields without technical complexity. Join the waitlist for early access.

Join the waitlist