Executive summary: The shift to high-yield savings alternatives

In 2026, the financial landscape is pushing European savers to rethink their cash management strategies. With traditional bank accounts frequently failing to outpace inflation, everyday investors are actively seeking high-yield savings alternatives to protect and grow their wealth.

The transition from legacy banking to innovative financial technology is driven by a clear demand for better returns and radical transparency. Here are the top three reasons why savers are abandoning low-yield accounts this year:

- Stagnant traditional yields: While institutions like Marcus by Goldman Sachs or Varo offer competitive rates, standard bank accounts still lag significantly behind inflation.

- Demand for flexibility: Savers want high returns without the strict lockups or penalties required by traditional Certificates of Deposit (CDs) offered by brokers like E*TRADE.

- Rise of accessible DeFi: Platforms like unflat bridge traditional savings and decentralized finance, automatically converting fiat to USDC to generate a 4-7% APY without requiring any crypto knowledge.

Comparing traditional vs. modern savings alternatives

Understanding the differences between government-backed bonds, traditional high-yield savings accounts (HYSAs), and modern stablecoin yield apps is crucial for optimizing your 2026 financial portfolio.

| Feature | Traditional HYSA & CDs | I Bonds (TreasuryDirect) | unflat App |

|---|---|---|---|

| Yield Potential | Variable / Fixed (often below 5%) | Inflation-adjusted (e.g., 4.03%) | 4-7% APY |

| Liquidity & Lockups | Penalties on CDs | Locked for 12 months minimum | No lockups or withdrawal fees |

| Underlying Asset | Fiat currency (FDIC insured) | U.S. Government Debt | USDC via Morpho Protocol (Non-custodial) |

Key criteria for evaluating high-yield options

Selecting the right savings alternative in 2026 requires balancing return potential with accessibility and safety. Investors must evaluate how quickly they can access their funds and what underlying mechanisms generate the yield.

While traditional bank accounts prioritize FDIC insurance, modern decentralized finance platforms like unflat offer superior returns through transparent on-chain lending. Understanding these trade-offs is essential for building a resilient financial portfolio.

| Asset Class | APY Potential | Liquidity | Risk Profile |

|---|---|---|---|

| Traditional HYSA | Variable (often < 5%) | High (Instant access) | Low (FDIC insured) |

| Certificates of Deposit (CDs) | Fixed (e.g., 3.90% - 5%) | Low (Penalties apply) | Low (FDIC insured) |

| I Bonds | Inflation-adjusted (e.g., 4.03%) | Very Low (12-month lock) | Low (Gov-backed) |

| unflat App | 4-7% APY | High (No lockups) | Moderate (Non-custodial DeFi) |

APY and return potential

Annual Percentage Yield (APY) dictates how much your money grows over time, factoring in compound interest. When evaluating platforms, it is crucial to distinguish between fixed rates, like those offered by E*TRADE CDs, and variable rates found in money market accounts.

In 2026, unflat stands out by generating a stable 4-7% APY through the Morpho Protocol, bypassing traditional banking limitations. However, standard fiat yields remain highly sensitive to broader economic shifts.

- Federal Reserve interest rate decisions and monetary policy shifts.

- Inflation rates, which directly dictate the combined rate of Series I savings bonds via TreasuryDirect.

- Market borrowing demand and liquidity pool utilization rates in decentralized finance.

Liquidity and lock-up periods

Liquidity determines how easily you can convert your assets back into usable cash without incurring financial penalties. For everyday European savers, locking funds away for extended periods can be a significant drawback during unexpected emergencies.

While traditional CDs guarantee a fixed rate, they penalize early withdrawals. Conversely, unflat provides radical transparency and non-custodial control, ensuring your USDC funds remain fully accessible without any withdrawal fees.

- Instant access accounts (like unflat or standard HYSAs) allow daily withdrawals without penalty, ideal for emergency funds.

- Fixed-term lock-ups (like CDs) guarantee rates but charge early withdrawal penalties, reducing overall flexibility.

- Government I Bonds require a strict 12-month minimum lock-up, and cashing out before five years forfeits three months of interest.

Secure high returns with bank & government options

In 2026, savers have diverse options to protect their wealth against inflation. Traditional fiat-based savings alternatives provide stability, while modern decentralized finance platforms bridge the gap to higher yields. Choosing the right vehicle depends on your risk tolerance and liquidity needs.

Government bonds and high-yield savings accounts offer predictable, insured returns. However, innovative apps like unflat redefine earning potential by seamlessly converting fiat to USDC, unlocking superior decentralized yields without the traditional banking constraints.

| Platform | APY Potential | Minimum Deposit | Safety Features |

|---|---|---|---|

| unflat | 4-7% APY | None | Non-custodial, Transparent on-chain history |

| Marcus by Goldman Sachs | Variable (Market rate) | None | FDIC Insured |

| TreasuryDirect | 4.03% (I Bonds) | $25 | U.S. Government Backed |

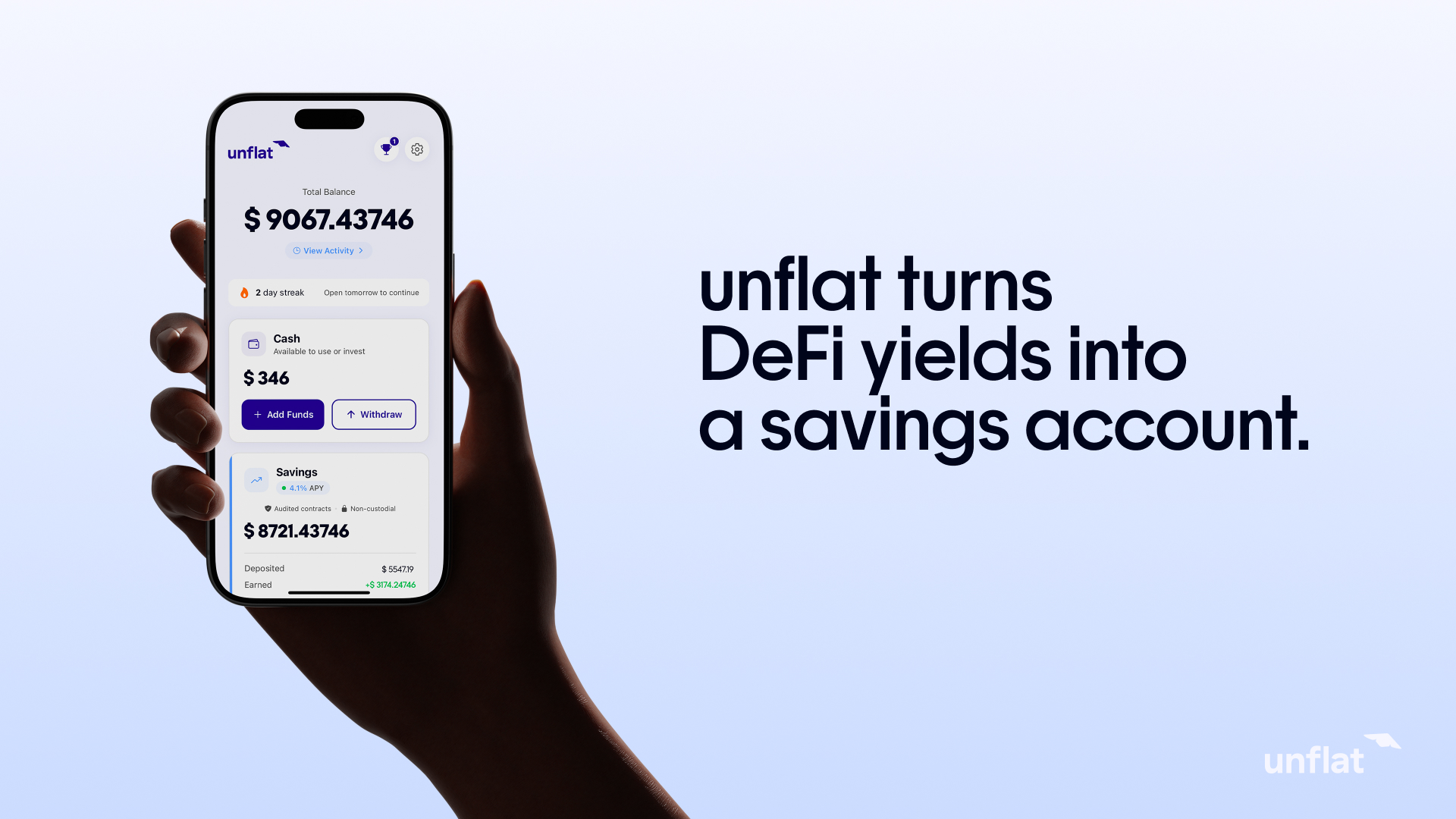

unflat: The ultimate modern savings alternative

For European savers seeking maximum yield with minimal friction, unflat is the premier choice. This mobile and web app automatically converts euro deposits into USDC, generating a stable 4-7% APY by lending funds via the Morpho Protocol on the Base chain.

Unlike traditional banks, unflat requires no crypto knowledge. It offers radical transparency with public on-chain links for every user, ensuring you maintain complete non-custodial control over your assets at all times.

- 4-7% APY generated through the secure Morpho Protocol.

- Zero lockups or withdrawal fees, ensuring daily liquidity.

- Non-custodial control of funds with transparent on-chain transaction history.

- Seamless fiat-to-USDC deposits via Coinbase Pay.

Marcus by Goldman Sachs and Varo

Traditional high-yield bank alternatives like Marcus by Goldman Sachs and Varo remain popular for their security and ease of use. Marcus provides straightforward savings and deposit products backed by 24/7 customer support and FDIC insurance.

Varo offers a compelling 5.00% APY on balances up to $5,000, though it requires meeting specific direct deposit and balance conditions. Both platforms are excellent for risk-averse savers prioritizing federal protection over maximum yield.

- Pro: FDIC insurance protects deposits up to $250,000.

- Pro: Varo offers up to 5.00% APY on lower balances (up to $5,000).

- Con: Varo's highest rates require strict direct deposit conditions.

- Con: Yields are highly sensitive to Federal Reserve rate cuts.

TreasuryDirect and E*TRADE

For those seeking fixed returns or inflation protection, government bonds and brokerage certificates of deposit are reliable choices. TreasuryDirect is the official portal to electronically buy U.S. Savings Bonds, offering a safe haven backed by the government.

Alternatively, brokerages like E*TRADE provide competitive, fixed-rate CD accounts. These allow investors to lock in an APY for a specific term, making them ideal for building a predictable CD laddering strategy.

- Series I Savings Bonds: Protect against inflation with a combined fixed and variable rate (currently 4.03%).

- E*TRADE CDs: Fixed-rate certificates of deposit with guaranteed returns for the entire term.

- Treasury Bills (T-Bills): Short-term government securities available via TreasuryDirect auctions.

High-yield opportunities in Crypto & DeFi

In 2026, the decentralized finance (DeFi) market continues to outpace traditional banking, offering a compelling high-yield alternative for everyday savers. By eliminating intermediaries, DeFi platforms distribute the majority of lending profits directly to users, transforming crypto into a reliable income asset class.

While traditional high-yield savings accounts are highly sensitive to Federal Reserve rate cuts, DeFi stablecoin yields remain robust. Platforms like unflat bridge this gap, allowing European savers to effortlessly access 4-7% APY through secure, non-custodial smart contracts without requiring any technical expertise.

| Feature | Traditional Savings (Banks) | DeFi Stablecoin Yields (e.g., unflat) |

|---|---|---|

| Average APY (2026) | Variable, sensitive to Fed cuts | 4-7% APY (Stable) |

| Underlying Asset | Fiat Currency (USD/EUR) | Stablecoins (USDC) |

| Custody & Control | Bank holds funds | Non-custodial (User controls funds) |

| Transparency | Opaque lending practices | Public on-chain transaction history |

Aave and decentralized lending protocols

Decentralized lending protocols like Aave allow users to earn interest on digital assets by supplying tokens to a liquidity pool. These supplied tokens automatically accumulate interest dynamically, with rates determined by real-time market borrowing demand and protocol governance parameters.

To protect lenders, Aave utilizes overcollateralized lending, ensuring borrowers deposit more value than they withdraw. While this provides security, navigating these protocols directly requires managing wallets, network fees, and smart contract approvals—complexities that apps like unflat abstract away for a frictionless experience.

- Connect a secure Web3 wallet to the Aave Labs interface.

- Select the specific digital asset or stablecoin you wish to supply.

- Approve the token transfer via a network transaction or gasless signature.

- Execute the supply transaction to transfer tokens into the Aave liquidity pool.

- Monitor your dynamically updating balance as interest accrues linearly over time.

Ensuring safety: FDIC, DeFi risks, and regulations

In 2026, chasing high yields requires balancing attractive returns with robust safety measures and regulatory compliance. Whether you choose traditional banking or innovative decentralized finance (DeFi), understanding how your funds are protected is crucial for long-term financial stability.

Traditional accounts rely on government-backed insurance, while DeFi protocols depend on smart contract security and overcollateralization. Here is how traditional insured platforms compare to non-insured decentralized alternatives.

| Feature | FDIC-Insured Platforms | Non-Insured DeFi Protocols |

|---|---|---|

| Protection Mechanism | Government-backed insurance | Smart contract audits & overcollateralization |

| Coverage Limit | Up to $250,000 per depositor | No formal coverage limit |

| Asset Types | Fiat currency (USD) | Crypto assets & Stablecoins (USDC) |

| Custody & Control | Bank holds funds | Non-custodial (User controls funds) |

Understanding FDIC insurance and bank safety

The FDIC protects money in traditional deposit accounts, covering up to $250,000 per depositor in the event of a bank failure. This government-backed safety net helps maintain public confidence in the U.S. financial system.

Financial authorities like CBS News and Bankrate consistently emphasize the importance of this protection when evaluating high-yield savings accounts in 2026. However, it strictly applies to fiat deposits, excluding crypto assets.

- Search for the institution in the official FDIC BankFind Suite.

- Look for the official 'Member FDIC' logo on the bank's website or app.

- Verify that the specific account type is covered (e.g., savings, checking, or CDs).

- Confirm the platform is a direct bank or uses legitimate sweep networks if it is a fintech app.

Navigating DeFi risks and smart contract vulnerabilities

While DeFi offers superior yields, it introduces unique risks absent in traditional banking. The primary concerns include smart contract vulnerabilities, where coding bugs could be exploited, and the potential de-pegging of stablecoins from their fiat counterparts.

Platforms like unflat mitigate these issues by building on battle-tested infrastructure like the Morpho Protocol and offering radical on-chain transparency. Still, users must adopt proactive strategies to safeguard their digital assets.

- Choose platforms utilizing audited and established protocols like Morpho or Aave.

- Opt for non-custodial solutions where you retain full control of your funds without lockups.

- Stick to highly liquid, reputable stablecoins like USDC to minimize de-pegging risks.

- Verify the platform provides public on-chain links for a transparent transaction history.

Frequently asked questions about high-yield alternatives

As savers look beyond traditional banking in 2026, navigating the landscape of high-yield alternatives requires absolute clarity. Whether you are exploring government-backed bonds or decentralized finance platforms, understanding the mechanics of these options is essential for maximizing your returns.

We have compiled the most common user queries regarding high-yield savings to help you make informed financial decisions. Below, you will find concise answers comparing traditional security with innovative platforms like unflat.

Top 5 queries on modern savings

- Are high-yield alternatives safe? Traditional options like CDs or money market accounts are highly secure, often backed by the FDIC up to $250,000. DeFi alternatives carry smart contract risks but mitigate them through overcollateralization and audited infrastructure.

- How does unflat compare to TreasuryDirect? TreasuryDirect offers I bonds with rates tied to inflation and strict lockup periods. In contrast, unflat provides a 4-7% APY on USDC with daily access, zero withdrawal fees, and radical on-chain transparency.

- What are the tax implications of DeFi yields? In most European jurisdictions, yields generated from stablecoin lending are subject to capital gains or income tax upon realization. You should consult a local tax professional to understand how automatic fiat-to-USDC conversions impact your specific liabilities.

- Is crypto lending worth the risk? For everyday users seeking higher returns, platforms utilizing battle-tested protocols like Aave or Morpho offer compelling rewards. By using non-custodial apps like unflat, you maintain full control of your funds without needing advanced crypto knowledge.

- How often do APYs change on these platforms? Traditional high-yield savings rates fluctuate based on central bank policies, while DeFi yields adjust dynamically according to market borrowing demand. However, stablecoin lending typically maintains a relatively consistent 4-7% APY range throughout 2026.

Start earning with unflat

Access DeFi yields without technical complexity. Join the waitlist for early access.

Join the waitlist