Top high-yield savings accounts and rates

In 2026, relying on traditional bank accounts means losing purchasing power to inflation. Finding robust alternatives to traditional savings is crucial for preserving and growing your wealth. High-yield options offer significantly better returns without sacrificing liquidity.

- Combat inflation: Outpace rising living costs with significantly higher APYs.

- Maximize passive income: Earn more on your idle cash effortlessly.

- Maintain liquidity: Access your funds quickly without lockups or withdrawal penalties.

- Diversify assets: Explore innovative platforms like unflat for stablecoin yields.

Comparing traditional vs. high-yield options

The gap between traditional banks and high-yield alternatives is widening in 2026. According to Bankrate and NerdWallet, high-yield savings accounts (HYSAs) offer APYs well above the national average.

Kiplinger Personal Finance emphasizes that these accounts often feature zero monthly fees. For even higher returns, DeFi platforms like unflat offer 4-7% APY by converting fiat to USDC, bridging traditional savings with decentralized finance.

| Feature | Traditional Banks | High-Yield Alternatives |

|---|---|---|

| Average APY | 0.01% - 0.40% | 4.00% - 7.00% |

| Monthly Fees | Often $5 - $15 | Usually $0 |

| Accessibility | Physical branches | Digital-first / Web apps |

Top competitor accounts overview

Several digital banks dominate the market with aggressive rates and modern features. Axos Bank offers the Axos ONE® bundle with up to 4.21% APY. In Europe, Openbank attracts users with promotional cash bonuses.

Meanwhile, N26 provides flexible instant savings directly within its budgeting app. While these are solid choices, they often require specific conditions to unlock the best rates.

- Axos ONE®: Pro: High APY and zero fees. Con: US-focused, requires specific direct deposit activities.

- Openbank: Pro: €200 sign-up bonus and 2.02% APY. Con: Requires direct debits and Bizum activation.

- N26: Pro: Seamless integration with Spaces and 2.26% APY. Con: Lower yield compared to DeFi alternatives like unflat.

Understanding bonds and certificates of deposit

Fixed-income alternatives like bonds and Certificates of Deposit (CDs) remain foundational for wealth preservation in 2026. While offering predictable returns, they require locking up capital, unlike flexible platforms like unflat.

Understanding the nuances between these traditional assets is crucial for balancing portfolio risk and accessibility.

- Bonds: Feature longer lock-up periods (up to 30 years) but can be sold on the secondary market for early liquidity, subject to price volatility.

- Certificates of Deposit (CDs): Offer fixed terms (3 months to 5 years) with strict early withdrawal penalties, making them highly illiquid.

- Yield vs. Flexibility: Both sacrifice daily access for guaranteed rates, contrasting with the no-lockup, 4-7% APY model of unflat.

Treasury bonds and government securities

Government-backed securities are incredibly safe investments backed by the government's full faith and credit. The Department of the Treasury issues these bonds, paying fixed interest every six months until maturity.

While highly secure, they lack the high-yield potential of decentralized finance, serving primarily as a conservative hedge against market volatility.

- Direct purchase: Open an account on the TreasuryDirect website to buy electronic bonds (minimum $100).

- Brokerage accounts: Use a registered broker to buy and sell government securities on the secondary market.

- ETFs: Invest in exchange-traded funds holding diversified government bond portfolios.

How to choose the right CD

Selecting the right CD requires balancing yield with your liquidity timeline. A popular 2026 strategy is building a CD ladder, dividing your money across multiple CDs with staggered maturity dates.

This approach ensures regular access to a portion of your funds while capturing the higher rates of longer-term commitments.

| Term Length | Typical Yield Expectation | Early Withdrawal Penalty |

|---|---|---|

| 6-Month | Moderate (tracks with HYSAs) | 30-90 days of interest |

| 1-Year | High (peak rates currently) | 90-180 days of interest |

| 5-Year | Stable long-term rate | 180-365 days of interest |

Cash management: MMFs and deposit insurance

Cash management accounts (CMAs) provide a compelling hybrid solution for 2026 investors, seamlessly blending the high yield of savings with the daily liquidity of a checking account. They automatically sweep uninvested cash into partner banks or money market funds to generate returns.

While traditional CMAs offer excellent flexibility, they often yield less than decentralized alternatives like unflat, which delivers a 4-7% APY without lockups. Still, CMAs remain a strong fiat-based option for everyday financial operations.

- Higher interest rates on idle cash balances compared to traditional checking.

- Expanded FDIC insurance through partner bank sweep programs.

- Standard checking features like debit cards, bill pay, and ATM access.

Money Market Funds explained

Money Market Funds (MMFs) are low-risk mutual funds that invest in highly liquid, short-term debt instruments. By tracking short-term interest rates, they offer a stable yield environment for conservative savers navigating 2026 market shifts.

European investors can explore MMF options through platforms like justETF.com for broad market analysis or MyInvestor for automated portfolios. Unlike unflat's stablecoin yields, MMF returns fluctuate directly with central bank policies.

| Feature | Money Market Funds | Standard Savings Accounts |

|---|---|---|

| Risk Level | Very Low (Investment product) | Extremely Low (Insured deposit) |

| Yield Potential | Moderate to High | Low to Moderate |

| Liquidity | High (T+1 settlement) | Instant |

Navigating FDIC and deposit insurance limits

Keeping your funds secure is paramount. The FDIC protects deposits up to $250,000 per depositor, per institution, per ownership category. This safety net ensures stability and public confidence during banking turbulence.

For balances exceeding this limit, strategic account structuring is essential. While DeFi platforms like unflat rely on transparent, non-custodial smart contract security rather than traditional insurance, fiat savers must actively manage their FDIC exposure.

- Open accounts across multiple unaffiliated FDIC-insured banks.

- Utilize different ownership categories (e.g., single, joint, and trust accounts).

- Leverage network deposit services like IntraFi to spread large balances automatically.

Robo-advisors and DeFi: Opportunities & risks

Modern wealth management in 2026 demands balancing aggressive yield generation with strict risk mitigation. Investors are increasingly shifting from traditional banking to automated algorithms and decentralized finance (DeFi) to combat inflation and maximize returns.

While platforms like unflat offer a streamlined, non-custodial bridge to DeFi yields, navigating this landscape requires understanding the inherent vulnerabilities of both smart contracts and algorithmic trading.

- Smart contract vulnerabilities: Bugs in underlying code can lead to permanent loss of funds.

- Algorithmic errors: Automated rebalancing might underperform during unprecedented market volatility.

- Regulatory uncertainty: Evolving 2026 compliance frameworks could impact platform accessibility.

- Liquidity crunches: Sudden market shifts can temporarily freeze asset withdrawals in poorly managed protocols.

Automated investing with robo-advisors

Robo-advisors optimize cash allocation by using algorithms to build and rebalance diversified, low-cost portfolios. This hands-off approach ensures your idle cash is continuously working, adapting to market shifts without requiring constant manual intervention.

Platforms like Indexa Capital Group excel in constructing automated portfolios with index funds, while Smart finance tools simplify budgeting and low-risk asset distribution.

| Feature | Traditional Wealth Management | Robo-Advisors |

|---|---|---|

| Management Fees | High (1.00% - 2.00% annually) | Low (0.15% - 0.50% annually) |

| Minimum Investment | Often $100,000+ | Low to Zero |

| Automation Level | Manual, advisor-dependent | Fully automated rebalancing |

The DeFi landscape and emerging platforms

Decentralized Finance (DeFi) presents a high-risk, high-reward alternative to traditional savings. By eliminating intermediaries, users can access superior yields, though this requires navigating complex protocols and assuming full responsibility for asset security.

While GreenFi focuses on fossil-fuel-free banking and Clapp offers fixed yields on crypto balances, unflat bridges the gap by automatically converting fiat to USDC for a transparent 4-7% APY on the Base chain.

- Public on-chain history: Ensure the platform provides radical transparency and verifiable transactions.

- Non-custodial control: Prioritize apps where you retain ultimate control over your funds.

- Unsustainable APYs: Treat double-digit, guaranteed returns as a major red flag for potential Ponzi tokenomics.

- Anonymous teams: Avoid protocols lacking a public, accountable founding team.

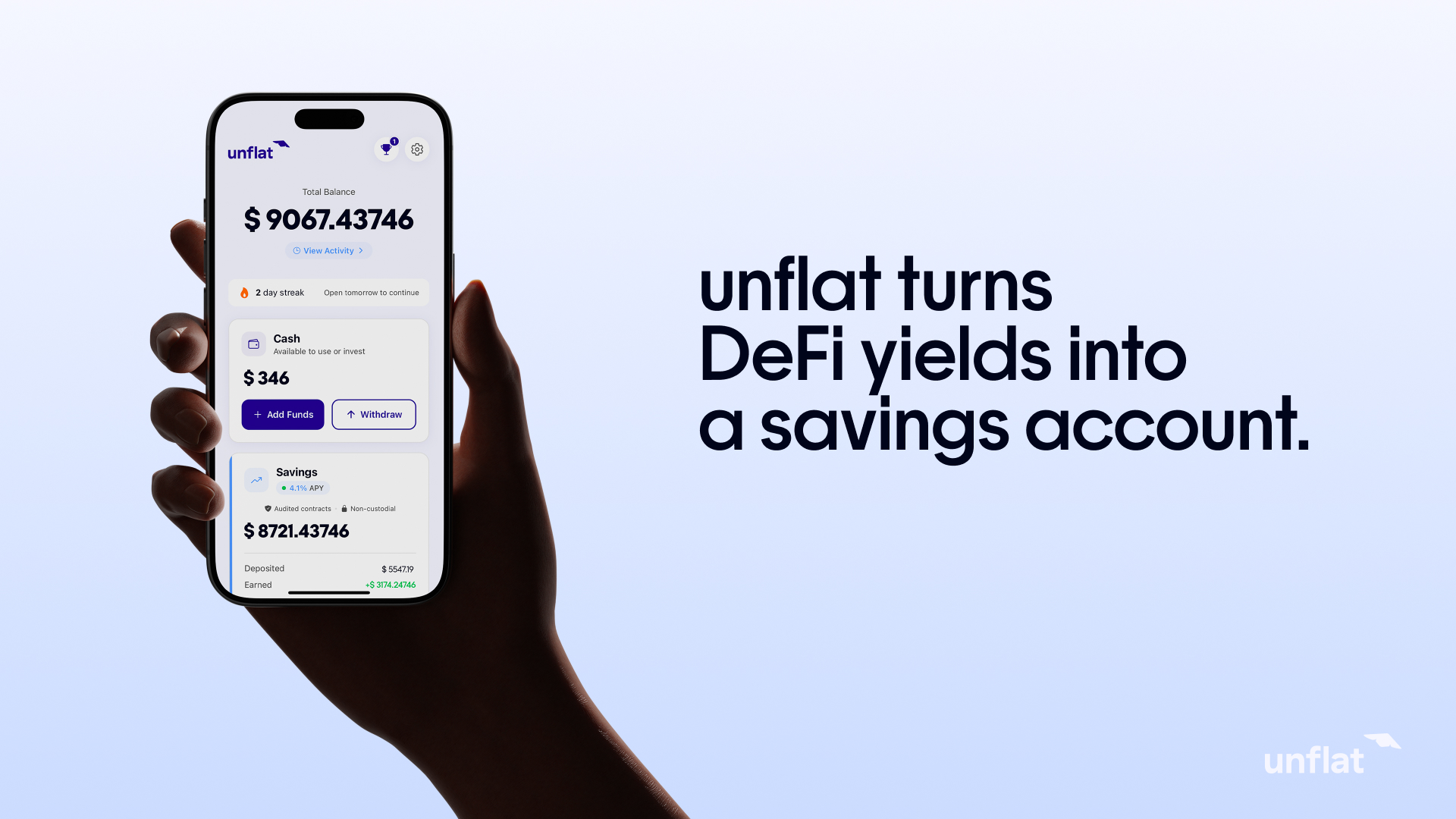

How unflat fits into your high-yield strategy

Navigating the complex 2026 financial landscape requires tools that balance security with competitive returns. unflat emerges as a seamless bridge between traditional fiat savings and decentralized finance. By eliminating the steep learning curve of crypto, it empowers everyday European savers to access sustainable yields without sacrificing liquidity.

- Consistent 4-7% APY: Generates stablecoin yield by lending funds via the battle-tested Morpho Protocol.

- Zero lockups or withdrawal fees: Maintain total flexibility over your capital with daily access.

- Non-custodial control: You retain absolute ownership of your funds, mitigating centralized exchange risks.

- Automated fiat-to-USDC conversion: Deposit euros effortlessly via Coinbase Pay without needing prior crypto knowledge.

Bridging the gap between fiat and DeFi

While platforms like N26 simplify budgeting and Clapp offers fixed crypto yields, unflat focuses on radical transparency. Operating on the highly efficient Base chain, it minimizes transaction costs while maximizing your earning potential. Every user receives public on-chain links to verify their transaction history in real-time.

| Feature | Traditional Banks | Pure DeFi | unflat |

|---|---|---|---|

| Average Yield (2026) | 2.00% - 4.00% | Highly Variable | 4.00% - 7.00% APY |

| Technical Knowledge | None | Advanced | None required |

| Fund Control | Custodial | Non-custodial | Non-custodial |

| Transparency | Opaque | Public ledger | Radical (Public on-chain links) |

Designed for the modern European saver

Built by a dedicated team based in Italy, unflat is specifically tailored to meet the needs of the European market. It strips away the complexity of managing wallets and private keys, offering a streamlined mobile and web application. This ensures your high-yield strategy remains both profitable and stress-free.

Frequently asked questions about savings alternatives

Navigating the 2026 financial landscape requires clarity. Here are the most common questions European savers ask when exploring high-yield options beyond traditional banking.

Are high-yield alternatives safe?

Safety depends on the asset class. Traditional accounts rely on FDIC or European equivalent insurance. Decentralized options carry smart contract risks. However, unflat mitigates this by using the battle-tested Morpho Protocol and offering non-custodial control, meaning you never surrender ownership of your funds.

Can I lose money in a CD?

You will not lose your principal if you hold a Certificate of Deposit to maturity. However, withdrawing early triggers early withdrawal penalties, which can eat into your initial deposit. Using a CD ladder, as suggested by Bankrate, helps maintain liquidity while capturing higher rates.

How do MMFs differ from savings accounts?

Money Market Funds (MMFs) are investment products holding short-term debt, subject to market fluctuations and protected by investor compensation schemes. Conversely, High-Yield Savings Accounts (HYSAs) are direct bank deposits protected by deposit insurance, offering guaranteed principal but often lower yields.

What is the best alternative for short-term savings?

For immediate liquidity and high returns, stablecoin savings apps are leading the 2026 market. While N26 offers 2.26% on instant savings, unflat provides a 4-7% APY by automatically converting fiat to USDC, with zero lockups or withdrawal fees.

How does inflation affect my savings yield?

Inflation directly erodes your purchasing power. Your real yield is your nominal interest rate minus the inflation rate. If your bank pays 2% but inflation is 3%, you are effectively losing money. High-yield alternatives are essential to outpace inflation and achieve true financial growth.

Start earning with unflat

Access DeFi yields without technical complexity. Join the waitlist for early access.

Join the waitlist