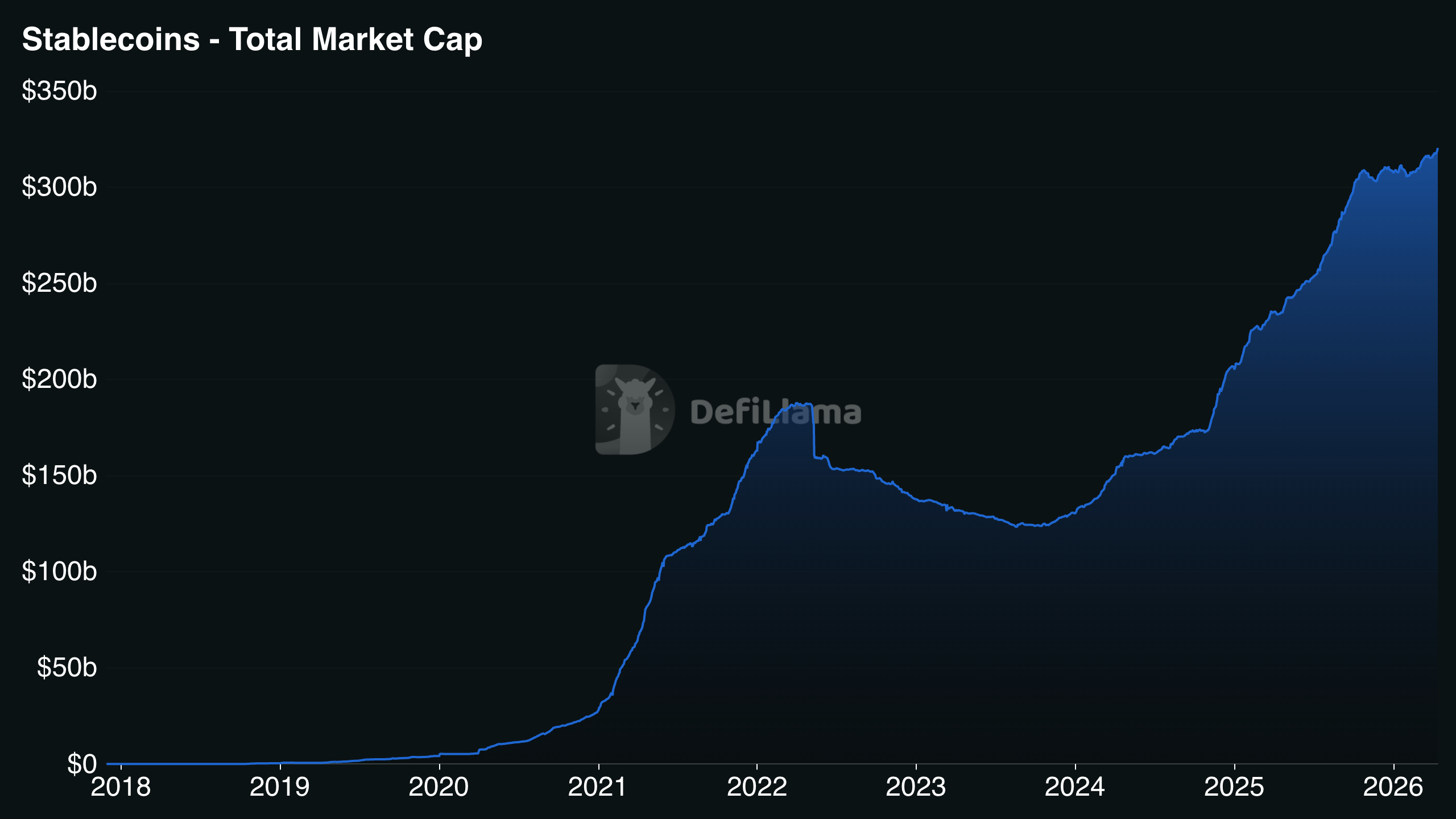

The stablecoin market just crossed $318 billion. In January 2026 alone, stablecoin networks settled more than $10 trillion in transactions, more than Visa over the same period.

And yet, if you ask the average European saver what a stablecoin is, you will most likely get a blank stare. Or a dismissive "that's crypto stuff, not for me."

This article is for exactly that person. We explain what stablecoins are, why 2026 is the year they became impossible to ignore, and how they fit next to the savings tools you already know. No jargon, no hype, no empty promises.

What a Stablecoin Is, in Plain Words

A stablecoin is a digital representation of a fiat currency (US dollar, euro, pound) that lives on a public blockchain like Ethereum, and holds a constant one to one value against the underlying currency. 1 USDC is always worth 1 dollar. 1 EURC is always worth 1 euro.

Three things to keep in mind.

- A stablecoin is not Bitcoin. It is not designed to appreciate. It is designed not to move.

- A stablecoin is not a bank transfer. It moves 24/7, in seconds, without touching SWIFT.

- A stablecoin is not a current account. It is a tool, not a guaranteed deposit.

In technical terms: it is a payment and settlement primitive. Translated for normal humans: it is a way to hold and move euros or dollars with the speed of a message and the transparency of a blockchain.

How Do Stablecoins Hold Their Value?

This is the right question. And the answer is simpler than it sounds: real reserves, held in low-risk assets, verifiable periodically.

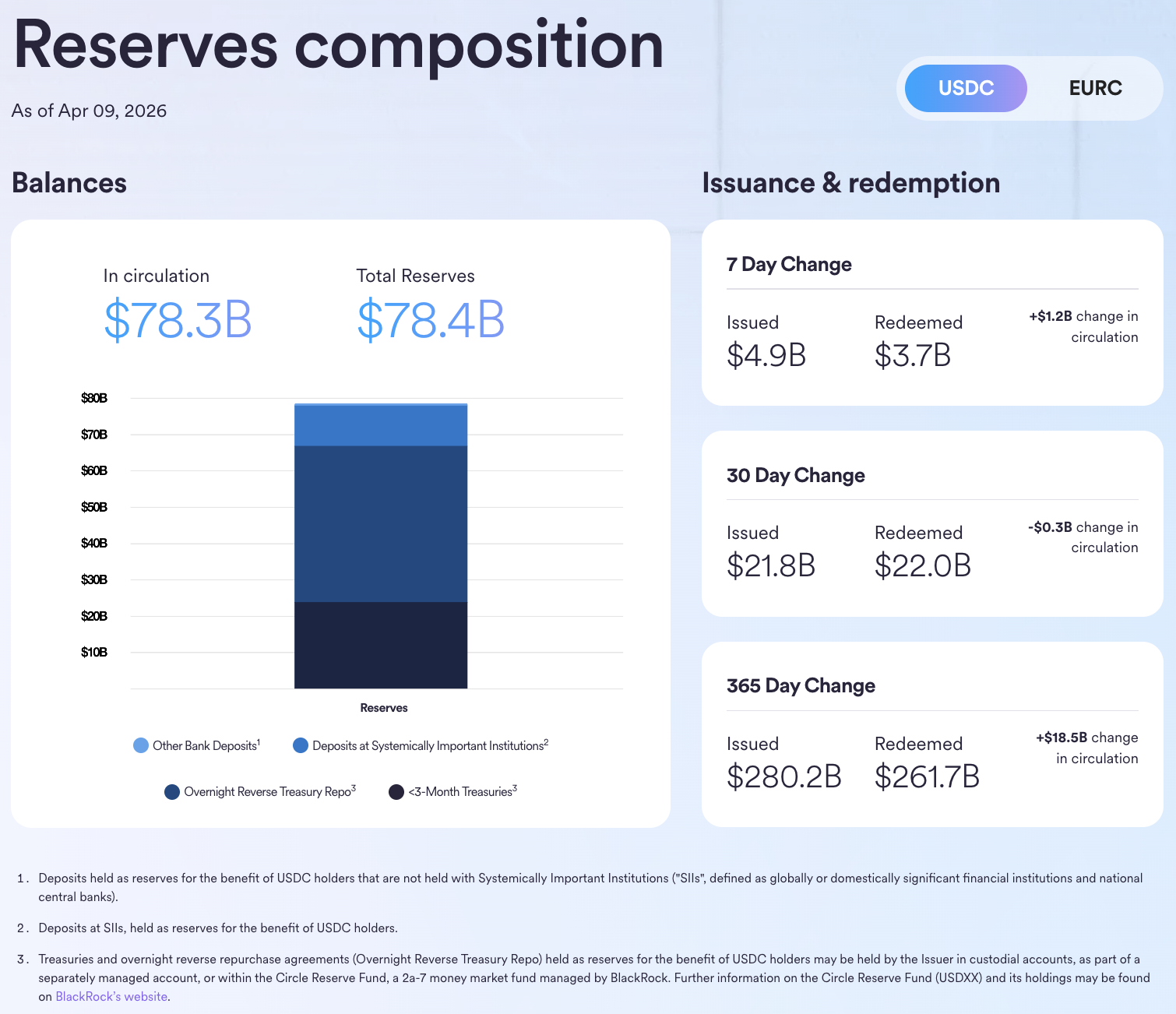

Take USDC, the stablecoin issued by Circle. For every USDC in circulation (currently $78.3 billion), Circle holds the equivalent in reserves:

- about 80% in short-dated US Treasuries (T-Bills);

- 20% in bank deposits at regulated institutions.

The majority of these reserves sit in the Circle Reserve Fund, an SEC-registered money market fund managed by BlackRock. Holdings are published every week on Circle's transparency page, and every month a Big Four accounting firm certifies that reserves exceed USDC in circulation. Circle has also been publicly listed on the NYSE (ticker CRCL) since June 2025: a full US public company, with SEC disclosure obligations.

The key word here is verify. You do not have to trust us: you can check. We put it this way at unflat: please don't trust us, verify what we're telling you.

Stablecoin, Bitcoin, Bank Account: Three Tools Solving Different Problems

It helps to be precise, because lumping "crypto" and "stablecoin" together is the first obstacle for newcomers.

Bitcoin Is a High-Volatility Investment

Bitcoin's price can swing 20% in a week. It is a long-horizon accumulation asset for people who can accept significant drawdowns. It is not a current account replacement, and it is not a stablecoin.

A Current Account Is Stable, but Hardly Generous

According to ECB statistics updated February 2026, the average rate on overnight household deposits in the euro area is 0.25%. Locking funds for twelve months gets you 1.77%. Meanwhile, Eurostat data (March 2026) puts euro-area inflation around 2.1%. In real terms, cash sitting on a current account loses purchasing power every year.

Stablecoins Can Generate Yield, with Different Risks

Depositing USDC into decentralized lending protocols like Morpho Protocol, you can earn variable yields that over the last twelve months have moved in a 4% to 7% APY net range. This is the mechanism unflat uses behind the scenes for its users: up to 7% APY, depending on vault and market conditions.

This is not a bank account. Yields are variable and market-dependent. Deposits are not covered by deposit guarantee schemes (FITD in Italy, equivalents across the EU). Never deposit money you cannot afford to lose.

The DeFi-specific risks are three: smart contract risk (bugs in the code), depeg risk (the stablecoin loses its anchor to the underlying), and protocol risk (the lending platform runs into a solvency issue). They are different risks from those of a bank, not necessarily bigger ones.

The question is not "either / or". It is how to diversify across these three tools based on your risk profile and time horizon.

Why 2026 Is a Turning Point for Stablecoins

Until a few years ago, stablecoins were an insider topic. Three distinct dynamics (regulatory, institutional, market) have pushed them into the mainstream.

1. MiCA Is Fully Operational, and It Helps Retail

The EU's MiCA regulation (Markets in Crypto-Assets) has set a uniform framework for stablecoins across all 27 EU member states. By July 2026, all crypto-asset service providers must be fully compliant or cease operations in the EU.

For retail investors, this is a structural change. It means minimum reserve requirements, audit obligations, segregation of client funds from issuer funds, and a single EU licence valid across the Union. Regulation adds cost for issuers and raises the quality bar, reducing the space for the kind of disorderly failures seen in 2022. USDC and EURC are already fully MiCA-compliant.

2. Circle Is Publicly Traded

Circle's NYSE IPO in June 2025 marked both a symbolic and a substantive shift. The issuer of the world's second-largest stablecoin is now a US public company, with public financials, quarterly disclosure, and reserves managed by BlackRock. Two years ago, this level of institutional transparency simply did not exist.

3. Infrastructure That Moves More Than Visa

With a market above $318 billion and monthly transaction volumes exceeding Visa's, stablecoins are financial infrastructure in every sense. According to a report published by Standard Chartered in April 2026, the market could exceed $1 trillion by year-end 2026. Similar projections have been published by Bernstein and Citi over the course of the year.

Why Does the Euro Matter? USDC Today, EURC Tomorrow

If you are a European saver, a fair question is: why do I have to go through the dollar?

Today, most stablecoins are USD-denominated. But the picture is moving. EURC, Circle's euro stablecoin, has reached $450 million in market capitalization and represents roughly 70% of the entire euro stablecoin market. Ingenico has enabled EURC payments on 40 million POS terminals worldwide. Visa has integrated EURC settlement.

unflat is natively European: born out of Bocconi's B4i program and backed by TEF (Tech Europe Foundation), it currently runs on USDC because EURC vaults on Morpho do not yet have the liquidity depth required to deliver stable yields. EURC is on the roadmap. The goal is a fully euro-native experience: deposit in euros, earn in euros, withdraw in euros, without FX risk.

How Can You Use Stablecoins to Grow Your Savings?

If you read this far, you are probably asking: "okay, how does this actually work?"

With unflat the flow is four steps.

- You buy USDC through one of the regulated partners integrated in the app, or you send USDC directly on-chain if you already hold some in a wallet.

- You deposit your USDC into unflat.

- Funds are allocated to Morpho Protocol (over $6.9 billion in TVL, zero exploits since inception) and start generating yield.

- You withdraw whenever you want, no lockups, no penalties.

Interest accrues in real time and is visible in-app second by second. The wallet is non-custodial: you own your wallet, and you can verify where your funds are at any time directly on-chain. No seed phrases to manage, no manual operations: the experience is simple, but control stays with you.

If you want to understand the story and the vision behind the project, read what unflat is and how it works or explore our savings guides.

What Are the Real Risks to Know Before You Start?

An honest article cannot only talk about opportunity. The real risks are three.

Smart contract risk. The lending protocol's code could contain bugs. Morpho has been audited multiple times and has never suffered an exploit, but zero risk does not exist.

Depeg risk. A stablecoin could temporarily lose its anchor to the underlying, as USDC did in March 2023 during the Silicon Valley Bank crisis, when it briefly traded at $0.88 before returning to $1. MiCA coverage reduces this risk but does not eliminate it.

Protocol risk. Decentralized lending is overcollateralized (the borrower posts more collateral than they borrow), but extreme price moves can still generate residual losses.

Understanding the risks is not a deterrent. It is the condition for using the tool in an informed way.

Conclusion

Stablecoins are not the future, they are the present. With a $318 billion market, an operational European regulatory framework, and verifiable reserves managed by institutions like BlackRock, they represent a concrete way to think about savings, next to (not instead of) traditional tools.

Three takeaways.

- Stablecoins are fiat on blockchain, not speculative crypto.

- The EU MiCA regulation is raising the quality bar in the retail investor's favor.

- There are tools built specifically for the European saver, with no advanced technical skills required.

If you want to get started, discover how unflat can put your savings to work. If you want to keep learning first, our guides are a good place to start.

Questions? Reach out. Transparency is not just a value, it is our method.